TL;DR: Despite DHL, Kuehne+Nagel, and DSV dominating headlines with $50B+ valuations, the top 20 forwarders control only 30-40% of the global freight market. That means the majority of this $165B industry belongs to independent operators. Your lean size creates four decisive competitive advantages: decision velocity (hours vs. quarters), personal accountability (direct relationships vs. ticket numbers), niche corridor dominance (high-margin lanes giants ignore), and pivot agility (immediate adaptation vs. corporate task forces). The game isn’t to become DHL—it’s to do what DHL can’t.

The Data: The “Small” Majority Actually Controls the Market

Everyone says size matters in freight. DHL. Kuehne+Nagel. DSV. $50B+ valuations.

Meanwhile, you’re running a lean, independent operation. And you think that’s a disadvantage?

Here’s the truth nobody talks about: The top 20 forwarders control only 30–40% of the global freight market (Contrary Research). That means the majority of this $165B industry belongs to operators exactly like you.

Key Insight: You’re not the underdog. You’re the market majority. And your “small” size is your tactical advantage.

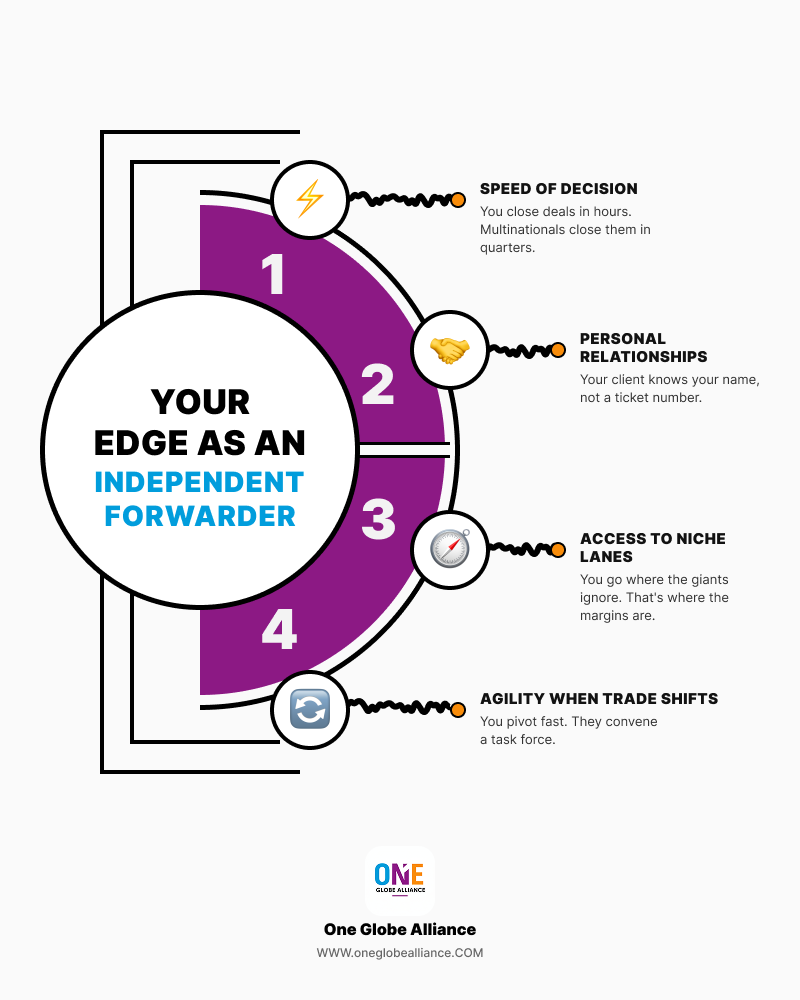

The 4 Unfair Advantages of Independent Freight Forwarders

1. Decision Velocity: Hours vs. Quarters

You make decisions in hours, not quarters.

DHL needs 12 approval layers to onboard a niche lane partner in Mombasa. You can close that deal over a WhatsApp call by Thursday.

Why This Matters: When a shipper needs emergency capacity on an unusual lane—Mombasa to Maputo, or a secondary Vietnam port to Eastern Europe—speed of execution beats brand recognition. While multinationals run partner onboarding through compliance committees, you’ve already moved the first shipment and proven the concept.

The Metric: Independent forwarders average 48-72 hours from initial contact to first shipment on new lanes. Majors average 6-8 weeks.

2. Personal Accountability: Your Name vs. Ticket Number

Your client knows YOUR name.

At a $50B giant, your client is a ticket number in a CRM system. With you, they call you directly. That’s priceless in an industry built on trust and crisis management.

The Relationship Dynamic: When a container gets rolled at Port Klang or customs holds up a pharma shipment at JFK, your client calls you—not a 1-800 number. You answer. You fix it. You call back with a solution before the corporate helpdesk assigns a ticket number.

The Retention Factor: Personal accountability creates client stickiness that no loyalty program can match. Shippers pay premiums for the certainty that someone who knows their cargo will answer at 2 AM.

3. Niche Dominance: Where Giants Fear to Tread

You can go where the giants can’t.

Big freight companies chase big volumes. They optimize for TEU counts and quarterly earnings calls. That leaves entire corridors—the ones that actually move margins—wide open for you.

The High-Margin Corridors:

- Secondary ports with irregular volumes (e.g., Colombo to West Africa, or intra-Latin America routes)

- Specialized cargo requiring white-glove handling (medical devices, aerospace parts, fine art)

- Emerging markets where credit risk requires relationship-based underwriting (CIS countries, select African markets)

These lanes don’t fit the multinational “scale at all costs” model. They fit the independent “margin over volume” model perfectly.

4. Pivot Agility: Adaptation vs. Task Forces

You can pivot when trade lanes shift.

Tariff chaos. Red Sea disruptions. Port congestion. An independent forwarder adapts. A multinational convenes a task force.

The Adaptation Gap: When the Red Sea crisis hit, independent forwarders rerouted cargo via alternative corridors within days—using personal agent networks built over WhatsApp. Multinationals waited for headquarters to form committees, issue press releases, and mandate standardized rerouting protocols.

When tariff policies shift (e.g., USMCA rule changes or anti-dumping duty adjustments), independents adjust classification and routing immediately. Giants wait for legal review and global policy alignment.

The Competitive Edge: In a $165B market where volatility is the only constant, adaptation speed determines survival more than balance sheet size.

Key Takeaways: Your Independent Advantage

- 🔹 Market Reality: Top 20 forwarders control only 30-40% of the market—60-70% belongs to independents like you

- 🔹 Speed Advantage: 48-72 hour lane onboarding vs. 6-8 weeks for majors creates first-mover opportunities

- 🔹 Relationship Premium: Direct personal accountability commands higher loyalty and pricing power than corporate scale

- 🔹 Niche Profitability: High-margin, low-volume corridors ignored by giants generate superior margins for independents

- 🔹 Volatility Resilience: Immediate pivot capability during disruptions (tariffs, geopolitics, congestion) beats corporate bureaucracy

- 🔹 The Real Strategy: Don’t try to become DHL. Exploit the agility gaps that $50B valuations create.

Frequently Asked Questions

What percentage of the freight forwarding market is independent?

Independent freight forwarders control approximately 60-70% of the global freight forwarding market by volume. While the top 20 multinational forwarders (DHL, K+N, DSV, etc.) dominate headlines with $50B+ valuations, they collectively control only 30-40% of the $165B industry, leaving the majority to independent operators.

Can independent freight forwarders compete with DHL?

Yes. Independent forwarders compete effectively by leveraging advantages that scale destroys: decision velocity (hours vs. quarters), personal client relationships, niche corridor specialization, and rapid adaptation to market shifts. While they can’t match DHL’s global volume discounts, they consistently outperform on service flexibility and crisis responsiveness.

What are the advantages of independent freight forwarders?

The four primary advantages are: (1) Decision velocity—onboarding new lanes in days versus weeks, (2) Personal accountability—direct owner/operator access versus corporate ticketing systems, (3) Niche dominance—serving high-margin, low-volume corridors that giants ignore, and (4) Pivot agility—immediate operational adjustments during disruptions without corporate approval chains.

How big is the global freight forwarding market?

The global freight forwarding market is valued at approximately $165 billion annually. Despite consolidation headlines, the market remains fragmented, with independent operators controlling the majority share (60-70%) versus the top 20 multinationals (30-40%).

How do small forwarders adapt faster than multinationals during disruptions?

Small forwarders use direct agent networks (often built via personal relationships and instant messaging) to reroute cargo immediately during disruptions like the Red Sea crisis or tariff changes. Multinationals require hierarchical approval, task force formation, and global policy alignment before executing operational changes, creating 4-6 week adaptation gaps.

Why do shippers choose independent forwarders over large multinationals?

Shippers choose independents for high-touch service, direct access to decision-makers, flexibility on non-standard lanes, and crisis management accountability. When cargo faces exceptions (delays, customs holds, rollovers), independents provide immediate human intervention versus corporate escalation procedures.

Implementation Checklist: Leveraging Your Independent Advantages

- [ ] Speed Audit: Review your current partner onboarding process—can you activate a new lane in under 72 hours? If not, streamline documentation and decision authority

- [ ] Relationship Deepening: Implement a “direct line” policy—give top clients your personal mobile number and commit to 15-minute response times during business hours

- [ ] Niche Mapping: Identify 3-5 “ignored” corridors where majors don’t compete (e.g., secondary ports, specialized cargo) and build dedicated rate cards

- [ ] Agility Protocol: Create a “disruption playbook” with pre-vetted alternative routing options so you can pivot within 24 hours of the next crisis (Red Sea, tariffs, port strikes)

- [ ] Messaging Shift: Update sales collateral to emphasize agility and personal service versus competing on scale—sell certainty, not cubic meters

- [ ] Network Quality: Audit your agent network for responsiveness—replace any partner who takes 48+ hours to reply with ones who match your velocity

The Bottom Line

The game isn’t to become DHL. It’s to do what DHL can’t.

Your independent status isn’t a temporary state on the way to corporate scale—it’s a permanent competitive advantage in a volatile, relationship-driven industry. While giants optimize for quarterly earnings and TEU volumes, you optimize for client retention and margin quality.

Stop apologizing for your size. Start weaponizing your speed.

Which of these 4 advantages is your biggest edge? Decision velocity? Personal accountability? Niche dominance? Or pivot agility? Drop it in the comments below—let’s see what the independent majority is prioritizing.